Currently, GST is not levied where the duty and GST amount on imported goods would in aggregate be less than $60 de minimis. This means goods with a landed New Zealand cost of less than $400, that do not attract duty, are not subject to NZ GST.

While the government will be taking with one hand, it will be a rare case of it giving with the other. Tariffs and border recovery charges will be removed from goods valued at or below $1000.

The growth in online shopping means there is a steadily increasing volume of off-shore purchased goods that are escaping New Zealand’s GST net. Some $870 million was spent online in 2017/18 on goods below $400 from offshore suppliers, with the value of this spending growing at approximately 12 percent annually.

The government estimates the change will bring in additional $66 million of GST revenue in the 2019/20 year, increasing to in excess of $100 million annually in subsequent years.

While the change is forecast to bring about significant extra amounts of GST revenue for the government, the Minister of Revenue has been quick to assert that the change is mostly about fairness to New Zealand’s retail sector and will help level the playing field.

Consumer impact

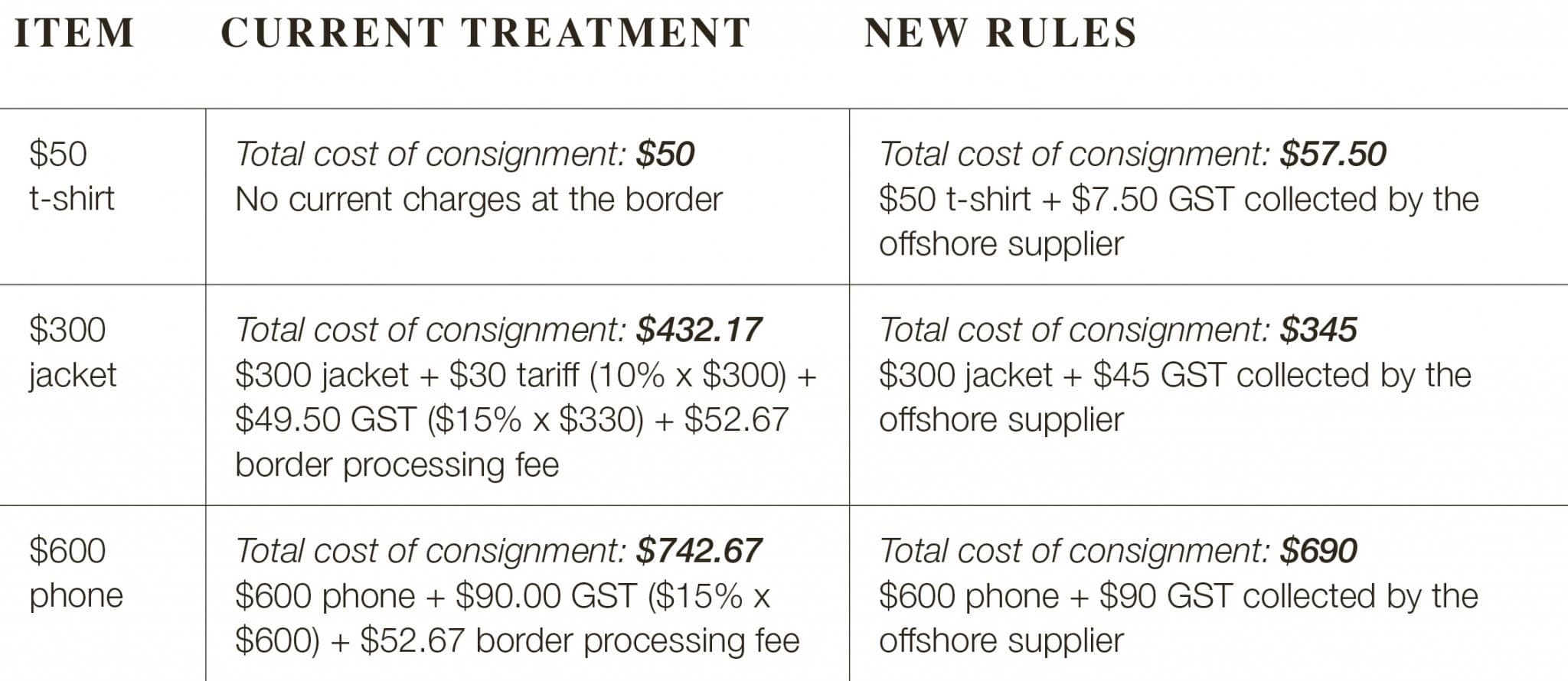

Given that the government will be removing tariffs/duties and border recovery charges, the GST change will not necessarily mean that all online purchases by consumers will be more expensive.

In fact, goods valued between $400 and $1000 would be cheaper, as would goods valued below $400 that exceed the current $60 duty + GST de minimis.

It will only be goods valued below $400 that do not currently have GST, duties and cost recover charges collected that would be more expensive under the proposal.

The table below from Inland Revenue illustrates the current and new treatment.

Often purchasers of imported goods get a surprise when they learn they have to pay GST, tariffs and cost recovery charges to Customs when their purchases reach New Zealand.

The changes will mean there is greater transparency and likely fewer surprises for consumers – what they pay for the goods when they purchase them online will be the actual price and there will be no hold-ups at the border.

If a consumer returns a purchase to an offshore supplier, the supplier will be responsible for returning the GST.

For goods valued at more than $1000, the current process whereby GST and any other duty is collected at the border by Customs will continue to apply.

Offshore suppliers will not be obligated to collect and return GST on supplies of goods made to New Zealand registered businesses.

Offshore supplier registration

Offshore suppliers will only be required to register for and collect GST if their total sales of goods and services to New Zealand exceed (or are expected to exceed) $60,000 in a 12-month period.

The government considers this offshore supplier registration model is the most effective mechanism to collect the GST at this time given the limitation of other potential approaches.

Other countries have adopted this model, including Australia, which introduced it in respect of low-value imported goods from July this year.

The government has acknowledged there will be some suppliers that will not comply with the rules and it aims to address non-compliance where it can through agreements it has with other countries around mutual co-operation and information sharing.

The obligation to register and return GST will also apply to both resident and non-resident electronic marketplaces, such as websites and internet portals used by suppliers to market and sell their goods.

Re-deliverers will also have a registration obligation.

Re-deliverers are businesses that are used by consumers when the supplier does not offer shipping to New Zealand.

The goods are instead sent to an overseas mailbox/hub which then in turn ships the goods to New Zealand.

Inland Revenue says that when non-compliance is detected, it will register the supplier for GST and issue a default assessment of the GST liabilities – essentially a guess of what the liability is – and the debt would then be registered with the New Zealand courts.

“Using our international agreements the debt would then be registered and pursued in the courts of the country that the supplier is based in.”

However, Inland Revenue then goes on to say that alternatively it could order a person based in NZ that owed money to a non-compliant offshore supplier to instead pay those funds to Inland Revenue.

It would be no surprise if the government issued further guidance for consumers on the new rules.

The new online GST arrangements will be an important adjunct to the rules introduced in 2016 that apply in respect of remote services (such as digital products, streamed music etc.) supplied by offshore suppliers.

The comments in this article are of a general nature and should not be relied on for specific cases, where readers should seek professional advice.